What is Purchase Order Management? Process & Best Practices

Efficient purchasing is conducive to healthy cash flow. The more effective your purchasing processes, the more profitable your business becomes.

Purchase order management helps businesses track and manage purchased goods, providing accurate visibility over the entire purchasing process and ensuring stock levels are optimised to prevent over-purchasing and underselling.

In this guide we explore the process of purchase order management, its role in a wider supply chain management strategy, and the best practices for optimised purchasing workflows.

Table of contents

- What is purchase order management?

- Why purchase order management is important?

- How the purchase order management process works

- The disadvantages of manually managing purchase orders

- Automating procurement: Purchase order management software

- Benefits of purchase order management software

- 7 essential purchase order best practices

- Tired of having the wrong amount of stock?

- Frequently asked questions

What is purchase order management?

Purchase order management is the process of creating, tracking, and managing purchase orders within a business. It’s a function of procurement that plays a vital role in effective supply chain management, ensuring optimal stock levels are achieved by balancing purchasing with accurate demand planning.

Effective purchase order management contributes to organisational efficiency, financial control, compliance, and positive supplier relationships. In doing so, it supports smooth operations and strategic decision-making within your business.

What is a supply chain?

A supply chain is the network of organisations, people, resources, technology and activities involved when creating and selling a product or service – from ordering raw materials to the end consumer.

Why purchase order management is important

Purchase order management is important because it provides a structured process for requesting, approving, and tracking purchases within an organisation. This ensures purchases are authorised, budgeted, and compliant with internal policies.

Here’s a quick breakdown of the benefits of effective purchase order management.

1. Manages order expectations

Because purchase orders detail the specifics of what is being ordered, there are fewer misunderstandings between the buyer and supplier, ensuring that both parties are aligned on expectations.

Having a clear purchase order process also helps with dispute resolutions. The PO document can be referred to if a disagreement needs to be settled and provides a reference point to compare what was ordered with what was received.

2. Prevents overspend and ensures healthy cash flow

Purchase order management allows for better budget management.

By requiring approval before purchases are made, purchase order management helps control spending and prevents unauthorised purchases. It also means you can track expenditures against budgets and allocate resources efficiently.

3. Improves supplier relationships

Clear and organised purchase orders enhance relationships with suppliers. Vendors appreciate receiving detailed and accurate orders, which can lead to smoother transactions, timely deliveries, and better service.

Importance of purchase order collaboration

Purchase order collaboration improves supply chain efficiency through real-time communication - reducing errors, minimising risks and increasing transparency. Purchase order collaboration also works to:

- Standardising processes: Streamlines regular practices such as inspections and speeds up problem resolutions

- Data sharing: All collaborators can view and updated purchase order information, ensuring all parties are on the same page when during order processing and dispatch.

4. Facilitates regulatory compliance

Controlled purchase order management ensures your business companies with regulatory requirements and internal policies. It provides a paper trail that can be audited to verify that purchases were made per established guidelines and used to guarantee accuracy during financial reporting.

5. Lifts operational productivity

According to Amazon’s 2024 Global State of Procurement Report, 44% of respondents listed efficiency and complexity as a challenge of procurement.

Streamlined procurement processes and clear communication facilitated by purchase order management save time and reduce administrative burdens. As a result, employees can focus on their core responsibilities rather than chasing down order details.

How the purchase order management process works

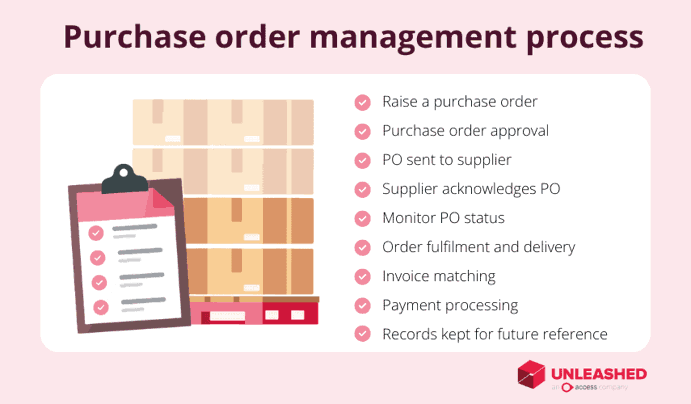

There are nine key steps in the purchase order management process:

- A purchase order is raised

- Somebody approves the PO

- The PO is sent to a supplier

- The supplier receives and acknowledges the PO

- The purchaser monitors the PO status

- Goods are delivered to and inspected by the purchasing company

- Invoices are matched to purchase orders

- Payment is processed by the supplier

- Records are kept for future referral

1. Creation of purchase order

The purchasing department or authorised personnel create a purchase order based on the requirements specified by the requester. This document serves as an official request to the supplier to deliver the specified goods or services.

2. Approval process

The purchase order may need to go through an approval process within the organisation to ensure budget adherence, compliance with purchasing policies, and correctness of details.

3. Dispatch to supplier

Once approved, the purchase order is sent to the supplier electronically or via mail. This communicates the organisation's intent to purchase and initiates the fulfilment process.

4. Receipt and acknowledgment

The supplier receives the purchase order and acknowledges it, confirming their ability to fulfil the order as specified. This step ensures alignment between the buyer and supplier regarding the transaction details.

5. Monitoring and tracking

Throughout the fulfilment process, the purchasing department monitors the status of the purchase order. This includes tracking delivery timelines, ensuring quality standards, and handling any deviations from the original order if necessary.

6. Receipt and inspection

Upon delivery, the receiving department checks the goods or services against the purchase order to verify quantity and quality. Any discrepancies are documented and addressed with the supplier for resolution.

7. Invoice matching

After successful delivery and inspection, the invoice from the supplier is matched against the purchase order and the receipt of goods or services. This ensures accurate billing and payment processing.

8. Payment processing

Once the invoice is verified and approved for payment, the finance department processes the payment to the supplier within the agreed-upon terms. In some cases, goods do not need to be paid for 30 or 60 days.

9. Record keeping

Finally, all documentation related to the purchase order – including the original request, approvals, purchase order itself, delivery receipts, and invoices – is maintained for record-keeping and auditing purposes.

The disadvantages of manually managing purchase orders

While manual purchase order management can suffice for smaller organisations with basic procurement needs, it can become inefficient and error-prone as businesses grow in both size and complexity – resulting in thinner profit margins and reduced customer satisfaction.

The main disadvantages of manual purchase order management systems include:

- Increased errors: Manual processes are prone to human error, such as typos, incorrect quantities or prices, and missed details. These errors can lead to delays in procurement, incorrect deliveries, and issues with supplier relationships.

- Too slow: Creating, reviewing, and processing purchase orders manually can be time-consuming. It involves handwritten or typed documents that need to be physically circulated for approvals, which can slow down the procurement cycle.

- Limited visibility and tracking: Manual systems often lack real-time visibility into the status of purchase orders. It can be difficult to track the progress of orders, monitor delivery timelines, and anticipate potential delays without automated tracking systems.

- Difficulty in scaling: As businesses grow or experience fluctuating demand, manually managing purchase orders becomes increasingly challenging. Handling a larger volume of orders manually can strain resources and increase the risk of errors.

- Lack of control and compliance: Manual processes may lack robust controls and compliance measures. It can be harder to enforce purchasing policies, approval workflows, and budget controls consistently across the organisation.

- Communication challenges: Manual systems rely on physical documents and verbal communication, which can lead to miscommunication or delays in conveying important information between departments, suppliers, and stakeholders.

- Audit and reporting issues: Gathering and maintaining accurate records for auditing purposes can be cumbersome with manual systems. Retrieving historical data, tracking changes, and generating comprehensive reports may require significant manual effort.

- Higher costs: While the initial investment in automation may seem high, manually managing purchase orders can incur hidden costs over time. These include labour costs associated with manual data entry, processing delays, and potential penalties for supplier errors.

- Poor supplier relationship management: Manual processes may hinder effective communication and collaboration with suppliers. Delayed or inaccurate purchase orders can strain relationships and impact supplier performance and reliability.

- Risk of data loss: Physical documents can be misplaced, damaged, or lost, leading to disruptions in procurement operations and potential data security risks if sensitive information falls into the wrong hands.

7 essential purchase order management best practices

Effective purchase order management can be achieved by adhering to industry best practices.

By implementing the strategies below, you can enhance your ability to manage purchase orders efficiently, leading to reduced costs, stronger supplier relationships, and a lift in overall operational effectiveness.

1. Standardise your processes

Every organisation should establish standardised procedures for creating, approving, and processing purchase orders. Clear guidelines outline who can create purchase orders, approval hierarchies, and steps for handling exceptions or urgent orders.

Consider utilising purchase order management software or enterprise resource planning (ERP) systems to automate and centralise the purchase order process. These can help generate purchase orders, track approvals, monitor order status, and facilitate communication with suppliers.

Implement structured approval workflows based on predefined rules such as approval limits, departmental budgets, and authorisation hierarchies. Ensure timely approvals to prevent delays in procurement and maintain compliance with policies.

2. Invest in automated PO management software

It’s crucial to have systems that monitor and track the status of purchase orders from creation to receipt of goods or services.

Utilise purchase order management software to automate routine tasks such as generating purchase orders, routing approvals, and sending notifications to stakeholders.

80% of respondents to Amazon’s State of Procurement report said they were considering integrating AI into their procurement processes within the next two years. AI-driven reporting functionality, such as Unleashed’s Advanced Inventory Manager, can help you accurately forecast sales demand to optimise purchasing.

3. Collaborate with internal stakeholders

Foster clear and open communication channels between departments involved in the procurement process, such as purchasing, finance, receiving, and suppliers. Ensure stakeholders are informed of order statuses, changes, and potential issues promptly.

Clarify roles and responsibilities to avoid delays or misunderstandings, and don’t forget to allocate vendor management to a specific team or individual.

4. Keep track of your suppliers

Some studies have shown that disrupted supply chains can cause a 62% financial loss, while a 2023 PWC survey found that supplier relationship management was the second-most important strategic priority of procurement departments. These stats both indicate that healthy relationships with reliable suppliers are essential.

Maintain up-to-date vendor information – including contact details, pricing agreements, delivery terms, and performance metrics – and regularly review vendor relationships to ensure alignment with organisational goals and quality standards.

5. Measure and review your performance

Regularly monitor and analyse purchase order processes to identify areas for improvement.

Analyse key metrics such as order cycle time, compliance with procurement policies, and supplier performance to optimise efficiency.

It’s also vital you foster a culture of continuous improvement within the procurement function. Try to gain a holistic understanding of your process efficiencies by soliciting feedback from stakeholders, suppliers, and end-users to use in conjunction with your KPI metrics.

6. Prioritise staff education

Be diligent in providing training and ongoing education to personnel involved in purchase order management. Ensure they are equipped with the necessary skills, knowledge of policies, and proficiency in using relevant tools to perform their roles effectively.

It’s also important your staff understand the importance of compliance, accuracy, and timely processing of purchase orders.

7. Keep a (digital) paper trail

Make sure you maintain comprehensive records of all purchase orders, including original requests, approvals, purchase order documents, delivery receipts, and invoices. This documentation is crucial for auditing purposes and resolving disputes.

Implement a cloud-based purchase order management system to ensure all information is securely stored online and always up-to-date and accurate.

Automating procurement: Purchase order management software

Purchase order management software boosts the efficiency and effectiveness of managing purchase orders by automating many aspects of the procurement process to reduce manual effort, minimise errors, and speed up the order creation process.

PO software provides a centralised platform where all purchase orders are stored digitally. This improves accessibility, allows for easy search and retrieval of past orders, and ensures that all stakeholders have real-time visibility into the status of orders.

10 key features of a purchase order management system

A purchase order management system typically includes several key features designed to streamline the procurement process and enhance efficiency:

- Purchase order creation

- Approval workflows

- Vendor management

- Document management

- Integration capabilities

- Real-time tracking

- Reporting and analytics

- Audit trail

- Automated notifications

- Security and access control

While not every PO management system will offer all these features – and many will offer these and more – it’s important to identify your specific needs when shopping for the right solution.

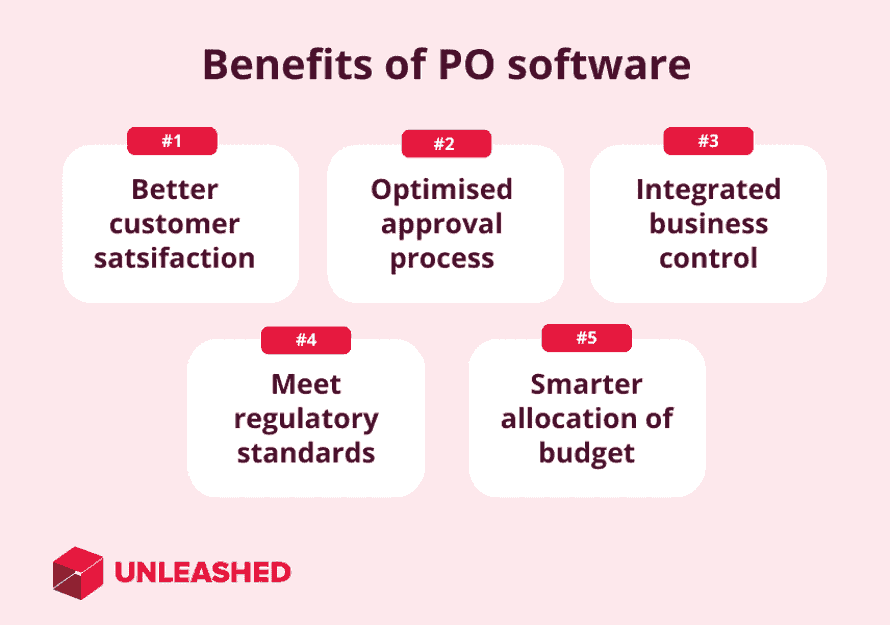

Benefits of purchase order management software

Purchase order management systems aim to lift procurement process efficiencies, driving smarter budget allocation and reducing administrative time to ultimately boost business-wide performance.

The key benefits of PO software include:

1. Lifts customer satisfaction

A recent survey found that shoppers’ main frustration (39%) with online shops is when a product is out of stock or low in stock. Real-time monitoring of purchase orders throughout the procurement cycle means users can track order statuses and delivery dates, and receive notifications for any delays or issues, allowing proactive management of orders.

2. Streamlined approval process

Purchase order management software facilitates streamlined approval workflows by routing purchase orders to designated approvers based on predefined rules (e.g., approval limits, departments) who can review and approve orders electronically. This speeds up the approval process and reduces bottlenecks.

3. Supports integrated business management

Many purchase order management solutions integrate with Enterprise Resource Planning (ERP) inventory systems and other financial software, ensuring seamless data flow between procurement, finance, and inventory management systems. This enhances overall operational efficiency and enables interdepartmental reporting and analytics.

With integrated PO software, you can generate reports on order history, spending patterns, vendor performance, and compliance with purchasing policies to gain insights which can help you spot cost-saving opportunities and improve procurement strategies.

4. Helps you meet regulatory requirements

An accurate compliance and audit trail helps enforce conformity with organisational purchasing policies and regulatory requirements. Details of all purchase order activities, including approvals and changes, are accessible and accurate – crucial for internal audits and compliance reviews.

5. Smarter spending allocation

Purchase order management software supports effective cost-control measures.

By improving accuracy in order creation, purchase order management software allows for monitoring spending against budgets and facilitating negotiation based on historical data. It also fosters better collaboration among departments involved in the procurement process and with external suppliers.

Tired of having the wrong amount of stock?

Unleashed is a trusted purchase order management system with features that help you streamline procurement and maximise cash flow.

Try Unleashed PO management software for free for 14-days to optimise and simplify your purchasing workflows.

Frequently asked questions

What is the OMS process?

The OMS (Order Management System) process refers to the full lifecycle of a purchase order, from creation to completion. It includes:

- A purchase order is raised

- The PO is approved

- The PO is sent to the supplier

- The supplier acknowledges the PO

- The purchaser monitors the PO status

- Goods are delivered and inspected

- Invoices are matched to POs

- Payment is processed

- Records are kept for future reference

This structured process ensures accuracy, compliance, and efficiency across procurement operations.

What are the four types of PO?

The four common types of purchase orders are:

- Standard Purchase Order (SPO) – Used for one-off purchases with known details (quantity, price, delivery).

- Planned Purchase Order (PPO) – Created in advance for future purchases, with estimated delivery dates.

- Blanket Purchase Order (BPO) – Covers multiple deliveries over time, often without fixed quantities.

- Contract Purchase Order (CPO) – A legal agreement outlining terms and conditions, without specific items listed.

These types help businesses tailor procurement to different supplier relationships and purchasing needs.

What is the PO process?

The PO (Purchase Order) process is a structured workflow that ensures goods or services are requested, approved, received, and paid for in a controlled and traceable manner. The nine steps are:

- Creation of the purchase order

- Internal approval

- Dispatch to supplier

- Supplier acknowledgment

- Monitoring and tracking

- Receipt and inspection of goods

- Invoice matching

- Payment processing

- Record keeping

This process supports financial control, supplier alignment, and audit readiness.

What are the 5 Ps of purchasing?

The “5 Ps of purchasing” refer to key principles that guide effective procurement strategy:

- Product – What is being purchased and its specifications.

- Price – The cost and value of the product or service.

- Place – Where the product is sourced or delivered.

- Promotion – Supplier incentives or terms.

- People – Stakeholders involved in the purchasing process.

This framework helps ensure purchasing decisions align with business goals and stakeholder needs.